Bottom Formation 1.2 - Capital Inflows

Disclaimer: This is not financial advice. Anything stated in this article is for informational purposes only, and should not be relied upon as a basis for investment decisions. Chris Keshian may maintain positions in any of the assets or projects discussed on this website.

To subscribe to my mailing list, input your email here.

To determine when to begin spot positioning in crypto assets, I look for bottom formation by watching signals from four key areas: Macro, Capital Inflows, Sentiment, and Technical Analysis. I arrived at these by regressing the change in price against a number of independent variables - a process I outlined in an earlier post titled Models . While each of these taken in isolation can be misleading, the confluence of all four help me to identify an approximate high time frame accumulation range, and therefore an appropriate time to begin spot positioning between market cycles.

The other posts in this series are:

Bottom Formation 1.0 - Intro

Bottom Formation 1.1 - Macro

Bottom Formation 1.2 - Capital Inflows

Bottom Formation 1.3 - Sentiment Analysis

Bottom Formation 1.4 - Technical Analysis

While I do think we are currently in the midst of a bear market rally, I believe we are in the early stages of this bottoming process. As such, I plan to track these signals more closely over the coming six months, and add to my spot positions as more of my conditions are met.

In this post, I will discuss the capital inflow metrics I track, reproduced below.

Amount of USDC and USDT in the System

Unrealized Net Profit/Loss

Market Value to Realized Value (MVRV)

Accumulation Trend Score

Adjusted Dormancy Score

Ratio Reset for GBTC/BTC and ETHE/ETH

Amount of USDC and USDT in the System

Given how onerous it is to move capital into and out of crypto, many investors choose to hold stablecoins when they “move to cash”, rather than converting back to fiat. While a certain percentage of this stablecoin market cap is put to work in DeFi (lending, liquidity provision, etc.), >50% of it is idle capital held on a wallet, waiting for the right time to re-enter spot positions. As such, I view stablecoin market cap as gravitational potential energy. Said another way, it is kindling for a crypto bull run, as I expect much of this capital to re-enter spot positions when investors feel more comfortable.

At the time of this writing, there is $137.15B worth of stablecoins in the system. As you can see from the chart below, this market cap changes based on what is happening in crypto - e.g. there was a massive drop in May 2022 during the Terra implosion. As favorable conditions return, I predict this stablecoin market cap to increase as more investors move capital into the space, and subsequently decrease as these stablecoins are traded for spot crypto.

source: DeFi Llama

Net Unrealized Profit/Loss (NUPL)

Unrealized Profit and Loss describes the aggregate profitability of the market held within the coin supply. NUPL is calculated by subtracting the realized cap from the market cap, and dividing the result by the market cap. This presents a measure of the total Unrealized Profit (+ve), or Loss (-ve) held within the coin supply as a proportion of the current Market Cap (described further in this article).

NUPL is one of the more powerful tools in on-chain analysis, and utilizes a concept called pricestamping, where each coin (or UTXO) is assigned a price (and thus USD value) when it is acquired, or spent on-chain. Using this, we can calculate the difference between the value at the current spot price, and compare it to the time of acquisition to calculate Unrealized Profit/Loss.

Coins acquired below spot prices hold an Unrealized Profit

Coins acquired above spot prices hold an Unrealized Loss

These tools allow for inspection of the relative and absolute profit or loss held within the coin supply, and split into various cohorts. As you can see from the chart below, this metric provides insight into when the market, on average, is in profit or underwater.

As you can see from the Bitcoin chart below, points during which price has traded below the average realized price present compelling buying opportunities. These zones show when price is trading below the average cost basis at which bitcoins were purchased.

MVRV Ratio

One metric I have used to track BTC from cycle-to-cycle has been Market Value to Realized Value (MVRV). MVRV has been nearly infallible as an indicator for how hot or cold the market is at any point in time. The ratio looks at the current price times supply (market cap) versus the cumulative “realized” value of “free float” coins - those that have moved in less than 5 years - at the price at which they last moved on-chain.

Market cap can stay the same when realized value spikes and vice versa. It’s a dynamic measure that accounts for flow. An MVRV that hits 3 has historically been a good point at which to sell, and a MVRV below 1 has historically been a good point to begin accumulating.

The MVRV ratio is an alternative approach to Market Cap as a measure of network valuation. Rather than using the last traded price and multiplying by the coins in circulation as seen in Market Cap, Realized Cap approximates the value paid for all coins in existence by summing the market value of coins at the time they last moved on chain. MVRV is simply the ratio comparing the two, i.e. MVRV = Market Cap / Realized Cap. It’s useful for getting a sense of when the exchange traded price is below “fair value” and is useful for spotting market tops and bottoms.

Accumulation Trend Score

The accumulation trend score shows a combination of the size of entities with respect to the number of new coins they have added or sold. Values closer to 1 (i.e., in darker colors) represent deep accumulation taking place. Large entities have been in this deep accumulation zone ever since the FTX collapse in November 2022. A similar accumulation pattern took place in both the 2018 and 2020 bottoms.

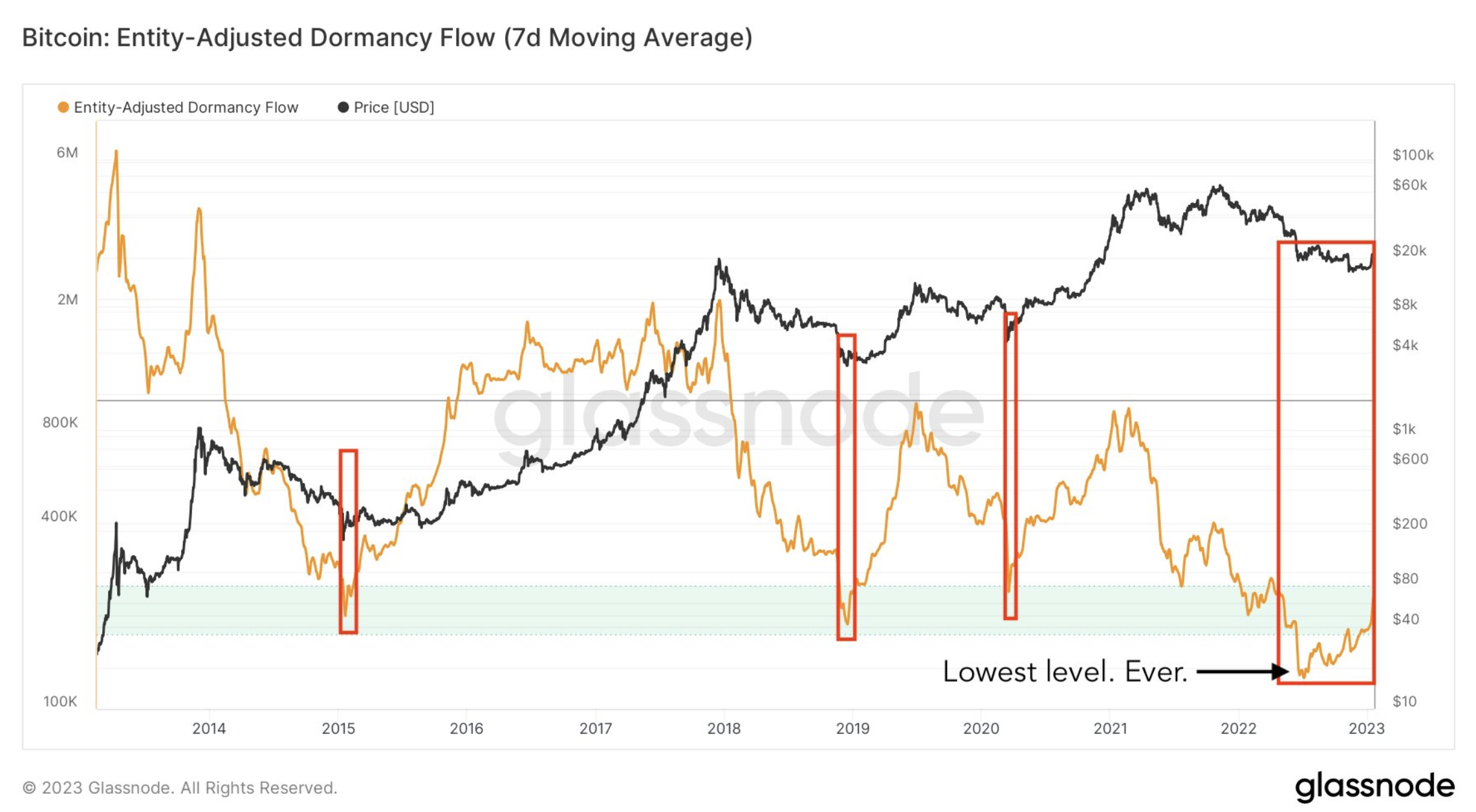

Adjusted Dormancy Score

Bitcoin entity-adjusted dormancy flow is the ratio of the current market cap to the annualized dormancy value. The lower the value, the longer the coins are held by investors. Dormancy flow came down to its lowest level ever during the FTX collapse, indicating that the speculative hands have been washed out and only the strong holders are remaining.

source: Glassnode

Ratio Reset for GBTC/BTC and ETHE/ETH

A final set of metrics I track (more loosely than the others) are the ratios of different derivative assets, most importantly GBTC/BTC and ETHE/ETH. Both GBTC and ETHE are trusts created by DCG. These trusts let customers who want exposure to Bitcoin and Ether, but do not want to hassle with private keys, obtain this exposure through their standard brokerage account.

Both of these assets traded at a premium to spot BTC and spot ETH before January 2021. This was because customer demand for this financial product exceeded supply, as there was significant retail interest in crypto. This opened an arbitrage opportunity, where investors could purchase spot assets and exchange them for GBTC or ETHE shares. I won’t go into further detail about this trade, but it became incredibly crowded while, simultaneiously, retail interest in these products decreased. At present, both of these trusts trade at a substantial discount to their underlying assets.

GBTC discount to spot = -42%

source: Y charts

ETHE discount to spot = -53%

source: Y charts

As the market begins to bottom, I suspect both of these assets begin to retrace the discounts they have established over the last two years, as retail interest returns and larger capital allocators see the merit in buying exposure to these majors at half price.