Active Portfolio Management for Liquid VC

Disclaimer: This is not financial advice. Anything stated in this article is for informational purposes only, and should not be relied upon as a basis for investment decisions. Chris Keshian may maintain positions in any of the assets or projects discussed on this website.

To subscribe to my mailing list, input your email here.

This is a seven-part series on FJ Labs’ investment process for liquid crypto:

As discussed in a previous post, one advantage to running a liquid venture capital fund in crypto is the ability to actively manage investment positions.

In previous posts I have outlined how we use regression to determine relevant metrics for 19 crypto verticals. I have also discussed how we use data dashboards to track these relevant category metrics.

In this post, I will discuss the advantages of investing in a liquid market – most notably, the ability to actively manage positions. Unlike in traditional venture capital, where investors must wait for a funding round to buy or sell their ownership, in liquid VC investors can exit or add to positions at any point.

Given the insight we have from our fundamental dashboards, we modify liquid positions in order to stay exposed to the leading projects in each vertical. Our portfolio management strategy is rooted in changes in fundamental metrics, which we track using our dashboard suite. While we have elected not to publish the specifics of this active management strategy, we have done some - strictly quantitative - work on active portfolio management, which will be the focus of this post. The below discussion is not indicative of the way we manage our portfolio, but instead is meant to provide a fun assessment of different active management strategies in liquid crypto.

Backtesting Active Management Strategies

In order to understand whether an actively managed liquid fund outperformed a passive buy and hold, traditional VC strategy, we performed a set of backtests. To do this, we had two datasets available:

Token Terminal Dataset, which tracks many fundamental metrics for a limited set of tokens (217). Tokens in the dataset have a selection bias, as they are sufficiently successful and have their historical data curated by Token Terminal. As such, any backtest involving this dataset must be qualified by this knowledge.

Coingecko Dataset, which tracks price and market cap of a large set of tokens (9,364 tokens) in a relatively unbiased way, by simply including any token that has been listed within the range of exchanges covered by Coingecko.

Because the Token Terminal dataset only includes the price history of successful tokens, there is an inherent selection bias that we would have not been able to infer ex-ante. To avoid this favorable-token bias, we chose to use the Coingecko dataset for backtests involving price and market cap, but used the Token Terminal dataset when more detailed fundamental metrics were warranted for specific assets.

Tokens in different market cap ranges behave differently, so we first segmented the space by market cap. The diagram below shows the distribution of market caps (in log USD) for tokens since 2013.

From this, we decided to use the following market cap ranges, which were derived from Coinbase:

Large-cap: >$10 billion. At the beginning of 2023, this consisted of only 6 tokens: BNB, Bitcoin, Ethereum, Tether, USDC, and XRP. Although Bitcoin and Ethereum were the only large-cap tokens in 2020, many more grew to fill the ranks in 2022 (19 large-cap tokens at peak)

Medium-cap: $1 billion to $10 billion. 2022 was a renaissance for medium-cap tokens, with 96 tokens that year compared to 30 in 2021 and 35 at the beginning of 2023.

Small-cap: $1 million to $1 billion. This segment rose during last market cycle, with 859 in 2021, 1,930 in 2022, and 1,804 at the beginning of 2023.

Mini-cap: <$1 million. The number of mini-cap tokens has been increasing over time, with 402 tokens in 2021, 509 added in 2021, and 1,568 added in 2022

Since medium to large cap tokens tend to have the most data available, we chose to perform our backtests on those categories.

Random Portfolio Construction

To prevent hindsight bias from clouding our asset selection process for this analysis, we decided to build 10 unique portfolios comprised of 25 randomly selected medium-to-large cap tokens. It is important to note that each of these 10 portfolios were selected completely at random, in order to generate strictly quantitative insights that were free from ex-post bias. In practice, as rigorous investors, we would expect to build a highly curated portfolio of assets based on research and data.

We then mapped the performance of our 10 random portfolios against the market. Our results from a simulation starting in 2020 are shown below.

The above graph shows:

Our 10 randomly constructed portfolios (portfolio_0 - portfolio_9)

Ethereum return

Bitcoin return

Non-rebalanced market-cap-weighted portfolio

Daily-rebalanced market-cap-weighted portfolio without Ethereum

Daily-rebalanced market-cap-weighted portfolio without Ethereum or Bitcoin

Bull Market Outperformance

Of our 10 simulated portfolios, 50% of them exceeded the average of the above five indices, while 50% of them underperformed. However, as we can see, many of the portfolios outperform even the highest index, Ethereum, at their peak. This indicates that diversification up to 25 tokens can sufficiently track the market, and that during a bull market this diversified portfolio of alt coins outperforms other liquid crypto investment strategies.

Bear Market Underperformance

If we look at a bear market, starting in 2022, we find that our 10 randomly selected portfolios consistently underperform.

This underperformance can be explained by the relative degree of sentiment-driven price action between smaller tokens and large-cap tokens like Ethereum and Bitcoin. Although Ethereum and Bitcoin themselves experienced volatility, the price of smaller tokens experienced far larger swings to the upside and downside. Therefore, even though a diversified portfolio can track indices over the long run after repeated cycles, they may actually consistently outperform or underperform during an individual bull run or bear run.

Ethereum Weighted Portfolio

To reduce the short-term beta of our portfolios, we may include some Ethereum-weighting (in this case, 20%) to our random portfolio in an attempt to temper volatility. While this approach does create a more similar return profile for our portfolios, it does not improve performance.

Turning to Actively Managed Strategies

From the above analysis we see that constructing a portfolio of up to 25 randomly selected tokens can provide diversified exposure to the market, as well as protection against uncorrelated risk. Additionally, adding Ethereum-weighting can further dampen idiosyncratic risk. That said, in no scenario is it ideal to track the market during a downturn. To avoid this, we turn to active management strategies, which offer the potential to lock in a return on our initial investment.

One possible active management strategy supported by established practice is selling at multiples. Since liquid crypto lacks the defined liquidity events of traditional VC, it is up to investors to tune the threshold around the multiples using domain-specific knowledge and acute awareness of market conditions.

To illustrate the potential of active management and proper tuning of multiples, we performed a suite of simulations. We took our 10 portfolios of 25 randomly selected medium-to-large cap tokens and sold tokens weekly when each individual token in our portfolio hit a 3x multiple. The total portfolio performance of this type of strategy is shown below.

As we can see, this form of management was able to capture gains from a market upturn while avoiding the downturn in 2022. This appears to be a suitable strategy when frothy market conditions are expected, or when multiples are expected to occur over a long period of time based on fundamentals.

To illustrate the importance of tuning the multiple, we simulated similar portfolio trajectories starting in 2020. If we set the multiple too low, we avoid a lot of potential upside as this approach does not sufficiently capture the degree of future market-driven hype or the real value added by crypto projects.

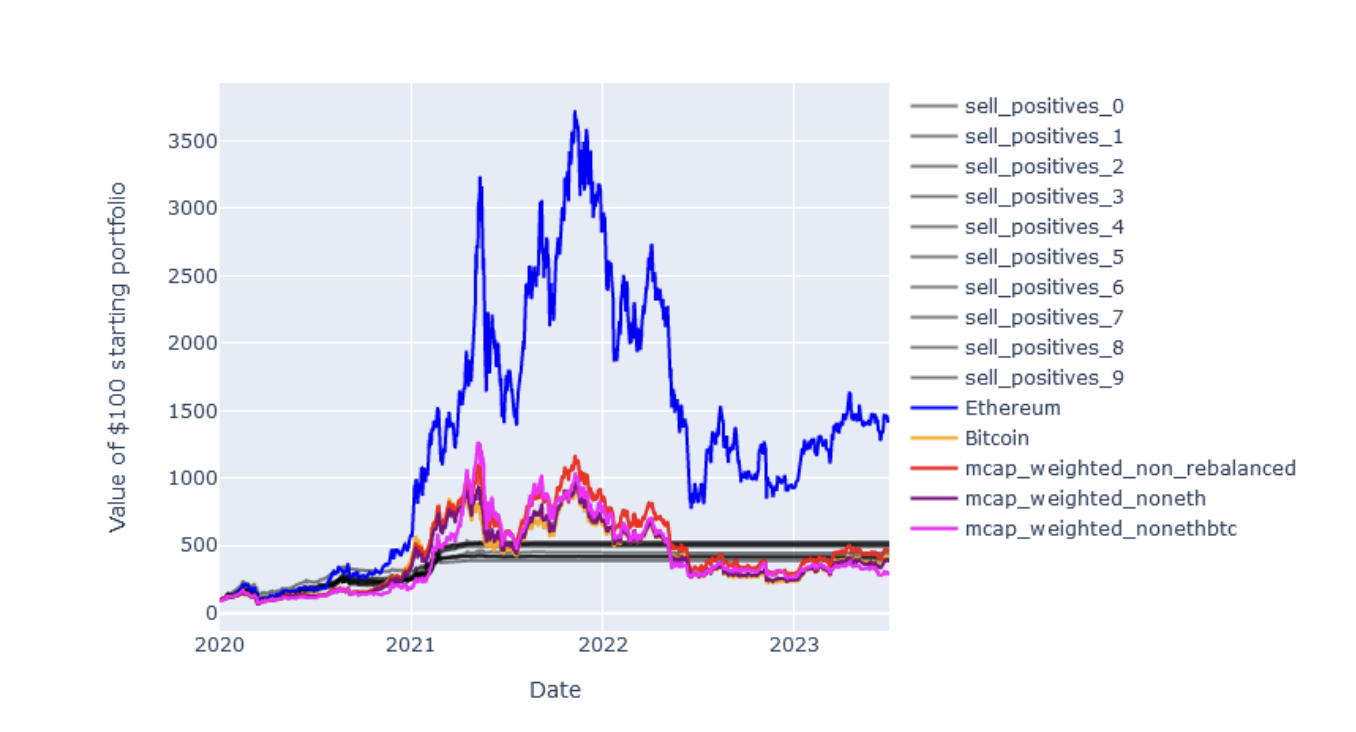

Selling Losers vs Selling Winners

Another active management strategy we studied was selling losers versus selling winners (i.e. rebalancing by selling assets that underperform vs rebalancing by selling assets that outperform). In this scheme, with monthly rebalancing, we either sell 10% of our equity in all negative performers and invest the proceedings into positive performers (momentum trading), or we sell 10% of our equity in all positive performers and invest the proceedings into negative performers (mean-reversion). Our backtest in a bull market (starting in 2021) shows that selling negatives can vastly outperform the market, while the median portfolio still performs at market level.

On the other hand, selling winners also appears to be a decent strategy, but does not perform as well as selling losers.

How could this possibly be true if the two strategies contradict each other? It turns out that both trend-following and mean-reversion exploit market behavior at relative maxima of the price curve. Trend-following amplifies the sentiment-driven growth that follows local maxima, while mean-reversion allows one to buy tokens at discount during temporary downturns.

Our Approach

For our internal purposes, rather than applying a blanket buy/sell approach to our portfolio, we have elected to use a fundamental valuation approach to determine when to sell. We built a model that arrives at a reasonable crypto asset price based on fundamentals and data. We use this model as a basis of comparison, and track how prices deviate significantly from these fundamental metrics. Given the sentiment driven hype cycles that fuel crypto bull markets, a strictly fundamental model - while disciplined - would cause investors to sell far too soon. As such, we use the quantitative work described above, along with an additional sentiment and narrative model to corroborate our decision to actively manage positions in our portfolio. As we think this approach has real edge for the foreseeable future, we have elected not to publish this method broadly.

Conclusion

The above backtesting process provides a useful raw, quantitative assessment of different portfolio management strategies. While informative, it is a blunt way to manage a liquid vc book in a space with such rich data access. Our model provides a more sophisticated, data-driven approach to managing a liquid book.